In the UK, Article 4 Direction is a legal direction or planning control that can be enforced by a local authority or council to restrict the number of HMOs (houses in multiple occupation) in a particular area. In a non-Article 4 area, automatic permitted development rights allow property owners to convert single homes or residential properties (C3 use class) into an HMO (C4 use class) without any need for planning permission. Article 4 removes this right, I know, as if we needed more constraints on creating good housing!

As a landlord or property investor, it is important to understand Article 4 and its restrictions, as it can be the breaking point between a good investment and a bad one. Whether you are investing in property for the very first time or already have multiple rental properties, having a solid understanding of Article 4 is important.

Why are Article 4 Directions Needed?

There are several reasons why Article 4 Directions for HMOs are needed.

HMO Article 4 Directions for C3 to C4 Change of Use

In most cases, C3 – C4 change of use directions are put in place in order to limit the number of HMOs in a designated area when there is a high concentration of them. In limiting the number of HMOs, local councils can control further proliferation and keep potential overcrowding under control.

For example, larger cities can often appear attractive to HMO investors given their large student populations, particularly students from overseas who generally pay more for good housing while studying. In addition, the cost of purchasing a property and the high cost of studying at university means that most students are likely to live in house shares. This makes students an ideal market for HMO investors. However, due to surging populations of students in cities, it’s important to have Article 4 in place to avoid overcrowding and quality loss in the area.

In many large cities such as Birmingham, London, and Manchester, an HMO Article 4 direction has been implemented.

HMO Article 4 Directions for Permitted Development

In some areas Article 4 directions for permitted development are in place to maintain the quality and character of places of historical or natural importance, such as conservation areas, national parks, world heritage sites and so on.

By introducing Article 4 and removing permitted rights, landlords seeking to buy or convert properties into HMOs must submit a planning application to the local authority. This means that the council is able to consider the impact on the local area before the development is authorised, such as impact on key public considerations like pollution, parking, overcrowding and noise.

For investors, this makes an Article 4 direction important when investing in any property in an Article 4 area, as there is no guarantee that your planning application will be successful. However, this does make HMO property valuation higher for a 6 bed because there is higher demand for the properties in article 4 areas. Speaking with a specialist such as HMO Designers will dramatically increase the likelihood of any planning approval for your application in an article 4 area.

HMO Checker takes the hassle out of Article 4

Find out if your property is in an Article 4 area using the #1 tool for HMO property sourcing & analysis

Try NowArticle 4 Areas in the UK

So, how do you know which areas in the UK have Article 4 Directions in place?

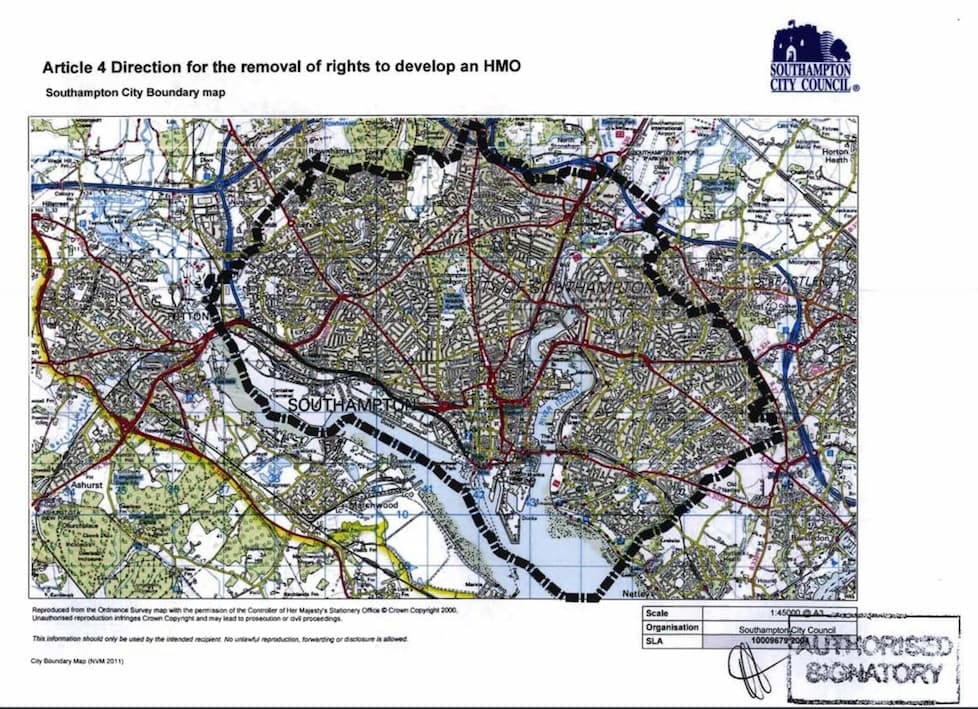

Unfortunately, there is not one single source online where you can easily find the UK areas that enforce Article 4 Directions. The easiest and most reliable way to find an Article 4 Area, is to look at the local authority’s website. Most local councils will have an “Article 4 Map” on their website which shows you the overall zone in a specific area with Article 4 in place. Failing this they will typically have a list of road names under article 4 instead.

Investing in HMOs and Article 4

Purchasing or investing in a property in Article 4 areas can feel risky when the investment hangs on whether or not planning permission will be granted. Therefore, there are some important considerations we recommend before investing in HMOs in Article 4 areas.

Speak to an HMO and Article 4 Expert

With any large investment, it’s also recommended speaking to a professional or expert who is familiar with HMO regulations throughout the UK. HMO Designers, for example, are a team of HMO architecture and regulation experts with a wealth of specific experience and know how to comply with local guidance and building regulations. If you are looking for more expert advice, please feel free to reach out to us.

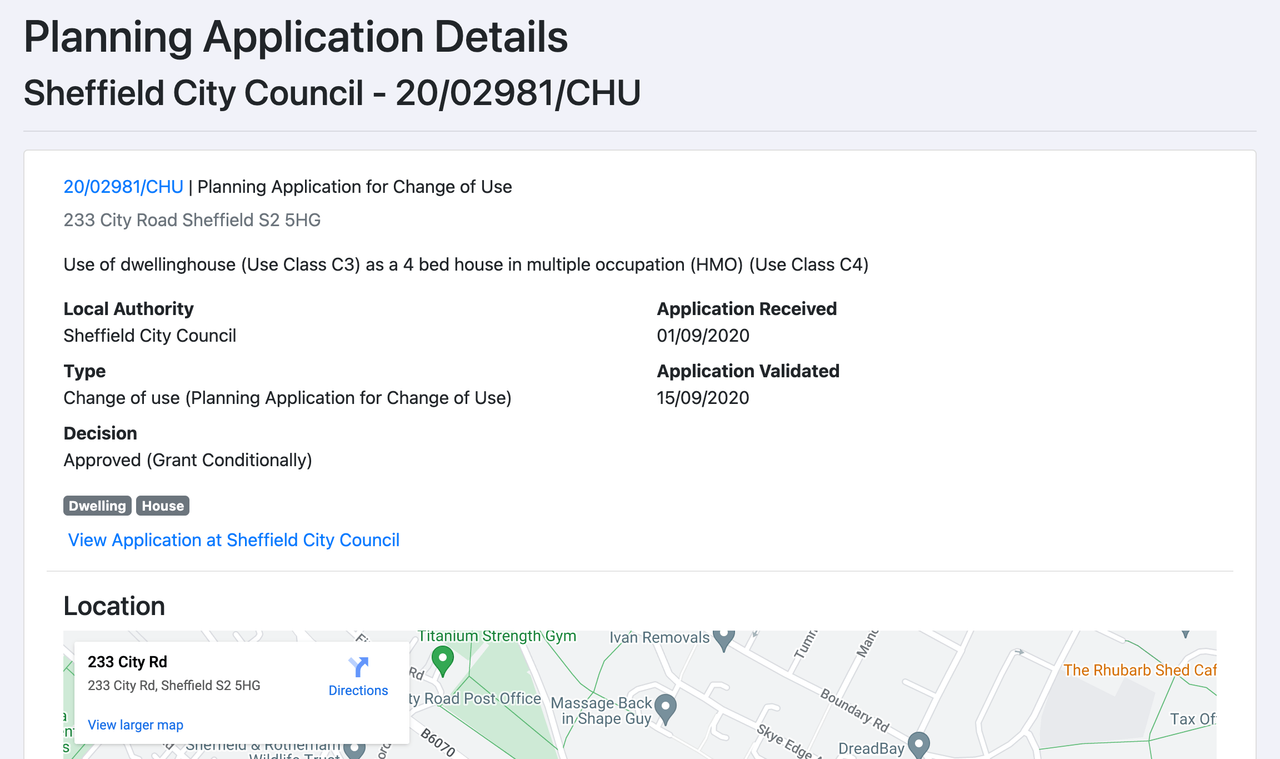

Look at Similar Planning Records

By assessing planning records on local council’s websites, you can potentially find properties that are comparable with the one you are looking to invest in to get an idea as to what applications have been accepted.

You can look for another property that has been through a similar process in the area to get further clarity on the likelihood of a similar outcome for yourself. You can try a website like Planning Explorer to find planning records for various local planning authorities.

Speak to Local Councils & Authorities

It is important to carry out your own research, including speaking to the local authorities in the area you are interested in, to get a better gauge on their specific regulations.

Local requirements and rules can vary from council to council, so it’s best to speak to them directly and individually. In some areas, they may ask you to prove how your investment will benefit the community, for example, whereas other authorities won’t require this.

Assess the Existing HMO Density

When you are carrying out your research and speaking to councils, it is worth asking what their current HMO density looks like. Most councils publish an HMO Density List which details the threshold for HMOs in the area in an effort to keep the overall percentage down.

Being higher or lower to the threshold would suggest the likelihood of an application being accepted.

Proof of Attempted Sale

Most councils will look to stimulate the growth of family and residential homes within their area in preference to landlords or HMO investors. Therefore, many councils can ask for evidence that the property in question has been marketed as a family house for at least 6 months with no success.

If you have previously marketed the house as a family home prior to considering converting to an HMO, this could have a positive impact on your application.